Quadratic and Cubic Terms in Linear Models.

In our weekly seminar, Robert Faff presented a paper with an OLS model with

the quadratic and cubic term effects. The dependent variable in this model

is the change in cash holdings (

The relevant part of the OLS model is

The results show that

You can see that the speed of adjustment depends on three coefficients and the

value of R.

First of all, I have to make a couple of assumptions because I don’t have the

full data. From the descriptive statistics, we know the meand (mopt) and

(sdopt) for opt_dev_norm) and a

t-distribution with 3 degrees of freedom (opt_dev_t). The latter will give

us larger outliers. Than we just calculate the cash holding change based on

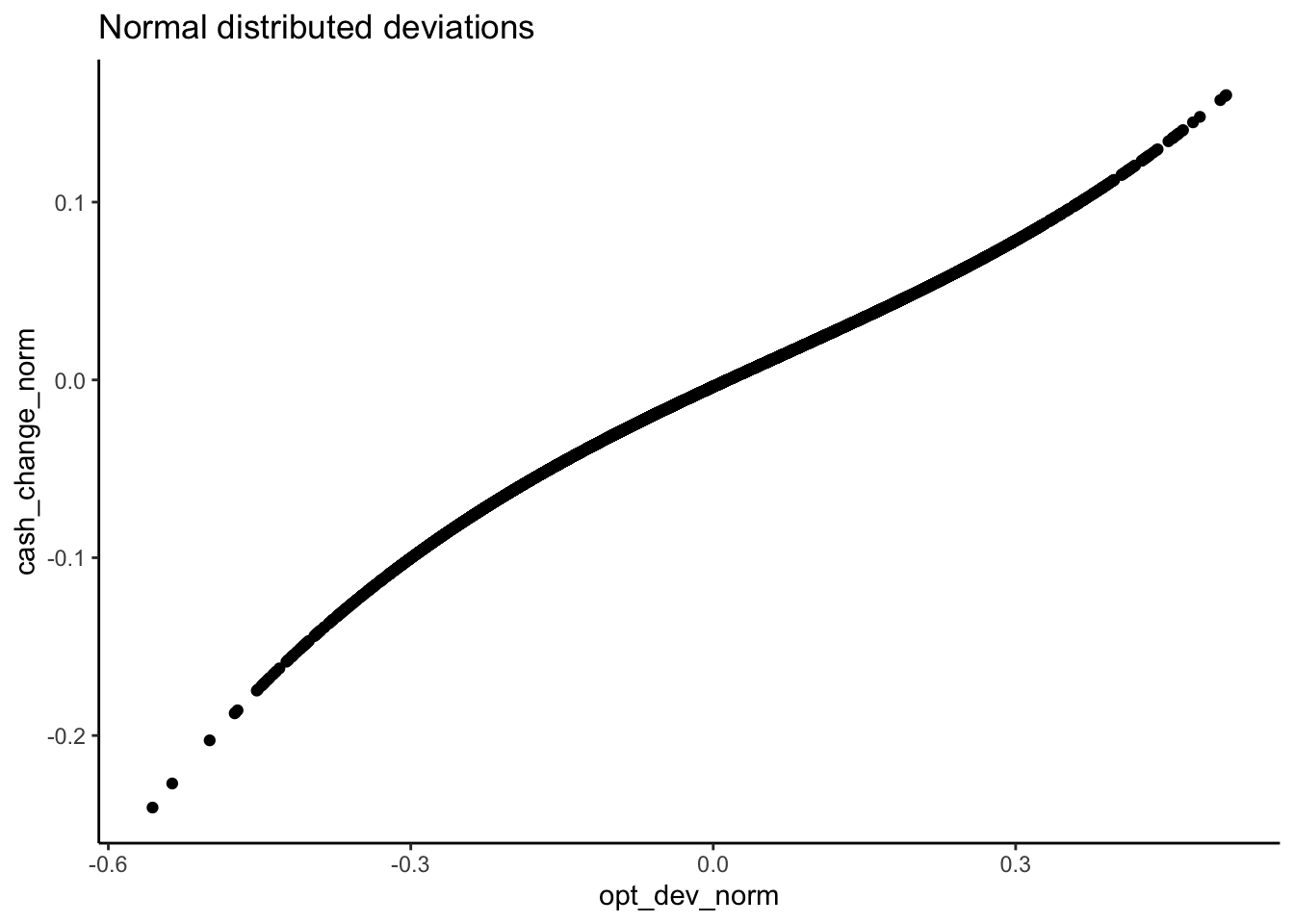

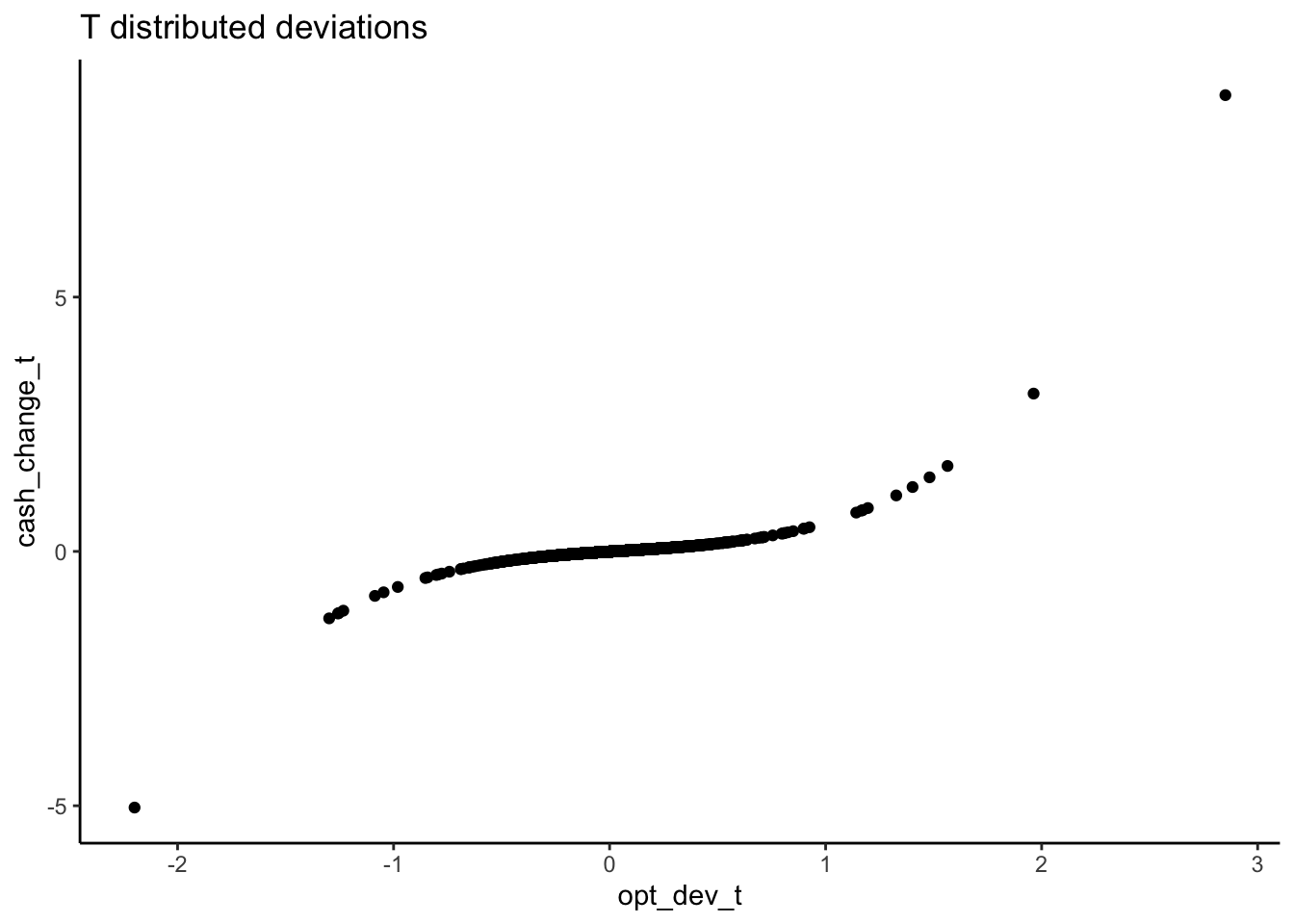

the ’s above and the OLS specification. Finally, you can plot the relation

between change in cash holding and the deviation from the optimal level.

What struck me was that the three regimes are much more clear with the t-distribution than with the normal distribution for the deviations. In other words, it looks like the extreme cases are doing a lot of work to identify the regimes.

require(ggplot2)## Loading required package: ggplot2mopt = -0.0026

sdopt = 0.1488

opt_dev_norm = rnorm(1e4, mopt, sdopt)

opt_dev_t = rt(1e4, df = 3) * sqrt(sdopt^2/3) + mopt

round(quantile(opt_dev_norm, probs = c(0.75, 0.5, 0.25)), 2)## 75% 50% 25%

## 0.1 0.0 -0.1round(quantile(opt_dev_t, probs = c(0.75, 0.5, 0.25)), 2)## 75% 50% 25%

## 0.06 0.00 -0.07cash_change_norm = -0.0038 + 0.2633 * opt_dev_norm - 0.0790 * opt_dev_norm ^ 2 +

0.3827 * opt_dev_norm ^ 3

normplot = qplot(x = opt_dev_norm, y = cash_change_norm) +

ggtitle("Normal distributed deviations") +

theme_classic()

cash_change_t = -0.0038 + 0.2633 * opt_dev_t - 0.0790 * opt_dev_t ^ 2 +

0.3827 * opt_dev_t ^ 3

tplot = qplot(x = opt_dev_t, y = cash_change_t) +

ggtitle("T distributed deviations") +

theme_classic()

print(normplot)

print(tplot)

Stijn Masschelein

Senior Lecturer in Accounting and Finance - Fellow in Center of Data Business Analytics

I am a lecturer in accounting at the University of Western Australia. I am interested in the role of (management accounting) information in decision making and risk taking. My research investigate how verifiable and subjective information supports formal and informal contracts. My interest is easily piqued and as a result I am involved in a wide variety of projects such as field applications in target setting and cost of quality, lab experiments on negotiations, markets, and risk taking, survey research on integrity and quantitative field studies in the banking sector. I developed experience in a range of statistical methods such as meta-analysis, (Bayesian) multilevel models, and simulations.